The reports from small pub/indie authors strongly support the report spike in ebook sales starting November 20th. ( From the comments on JA Konrath’s blog. see M. Louisa Locke’s post) I expect December results to be even better than November for ebook sales. However, from later comments over at JA’s blog, I am not expecting a large December to January spike in ebook sales.

I have seen some really bad articles on this month’s press release by people who just read the press release. Please look at the graphs. Each one tells a major story. I’m going to avoid talking numbers as I’ve seen a half dozen articles online that tried to confuse the reader and obscure conclusions. We’re going into chart reading mode after the introduction.

First, a few notes on the numbers:

1. AAP only has 14 of 88 publishers report ebook sales.

2. There are over 400 publishers

3. “Indie Authors” are not counted in the numbers

4. I estimated sales of indie books.

I really only have two data points on indie author market share, but they're quite useful for estimating the market share of small publisher/indie author ebook sales:

1. December 2009 ‘boutique’ books were 10% of ebook sales.

2. By scanning the December 2010 ‘bestseller lists,’ I conservatively estimate that 20% to 33.3% of ebook sales are small publisher/Indie Author.

3. I take the 20% market share for small publisher/Indie author for December 2010.

4. I then just interpolate linearly and I will extrapolate linearly until there are better numbers that I can reference.

The first graph has ebook sales. The blue line is the reported data for the 14 reporting AAP publishers. The green line is my overly conservative estimate of the real ebook sales. If anything, I think small publisher/indie author sales are walking away far faster than what I graphed… but I strive to never revise my numbers down.

For December, I expect the estimated ebook sales to break $70 million (possibly over $80 million, but note: my ‘official prediction’ is just over $70 million ebooks in December 2010). We’re trending for similar sales this month (January 2011). It is possible that for January 2011 we will temporarily exceed Hardcover sales (but only for a month with historically weak hardcover sales).

That comment transitions us to the second graph; I added trade book sales by my calculations (summing up AAP data). I see more and more web sites calculating trade sales by my method as the AAP numbers (what is published just does not add up). I also find that the annual numbers on ebook sales are always *higher* than the sum of the monthly reported AAP numbers (by about 3%).

The third graph is my calculation of ebook market share. I’ve seen numbers matching my own on the internet. Market share fluctuations are driven by ebook market growth and the incredibly noisy data of ‘trade books.’ My estimate is that we’ve broken 10% market share and we won’t look back. Pbook sales the first few months of the year are too weak to impact the trend. By July, ereader/ebook growth will ensure market share is well above 10% for ebooks.

Monthly comparisons with Noise bands:

A comment on the next charts: Monthly pbook sales are noisy. So I plot bands. Only when data is outside of a band does it mean anything… FYI, analyzing noisy data is my specialty, just be glad I’m not going into ‘design of experiment’ details.

Ebooks are at Mass Market Paper Back (MMPB) sales levels. With Small pub/Indie author sales, well past. The days of MMPB selling better than ebooks are over. Sadly the drop in MMPB sales points to the weakness of bookstores. B&N moved in toys which will forever impact midlist sales. Borders weakness is also going to drive fewer midlist purchases.

What about adult hardcover? Sales were good! It looks like stores delayed buying in October and made up the difference in November. I suspect a huge fraction of the buying was big box retailers. With the publisher drive to best sellers, I see the strong increase in hardcover sales a negative for midlist books.

Paperbacks were also weak. I expect that by the July 2011 data (not my July article, but when the AAP releases the July 2011 data) we will see ebooks passing paperback sales. Heck, probably passing adult paperback plus MMPB! I have some seasonal charts that show the change in sales clearer (later in this post).

I posted Children’s sales (combined hardcover and paperback) to illustrate that there is no evidence that ebooks have yet to affect these sales. But after starting my toddler on Ipad apps… I think this sector will take a hit. But this is a case where the tablets, including the color nook, will dominate. For kids, color and animation are the key (in my opinion). My daughter really has a leg up learning the ABCs from her IPad app…

Seasonal charts:

I graph the same data a different way to tell a different story. In these graphs, each year is a different line. The 1 is January, 3 is March, 5 is May, etc. This is so that we can see year over year growth or declines.

The first seasonal graph is ebooks. Please notice the constant year over year growth. Also notice the slope up in increasing. So much for any strawman arguments that growth will slow… There is some seasonal variation, but the trend, since 2008, is up and up. The next chart is a bar chart that shows the huge month of month growth. I expect slower growth once ebooks are above 40% market share. Until then, growth rates should increase.

Ok, now to show how pbook sales are dropping. I’ll start with paperbacks. Notice the orange line with circle markets started off 2010 ok and then fell? It looks like the K3 and color Nook took the wind out of adult paperback sales.

Looking at hardcovers, the data doesn’t look too bad (again, 2010 is orange with circle markers). Hardback sales have been poor since July. A slight stronger November doesn’t erase that. It looks like bookstore financial health is starting to impact hardback sales, but not drastically.

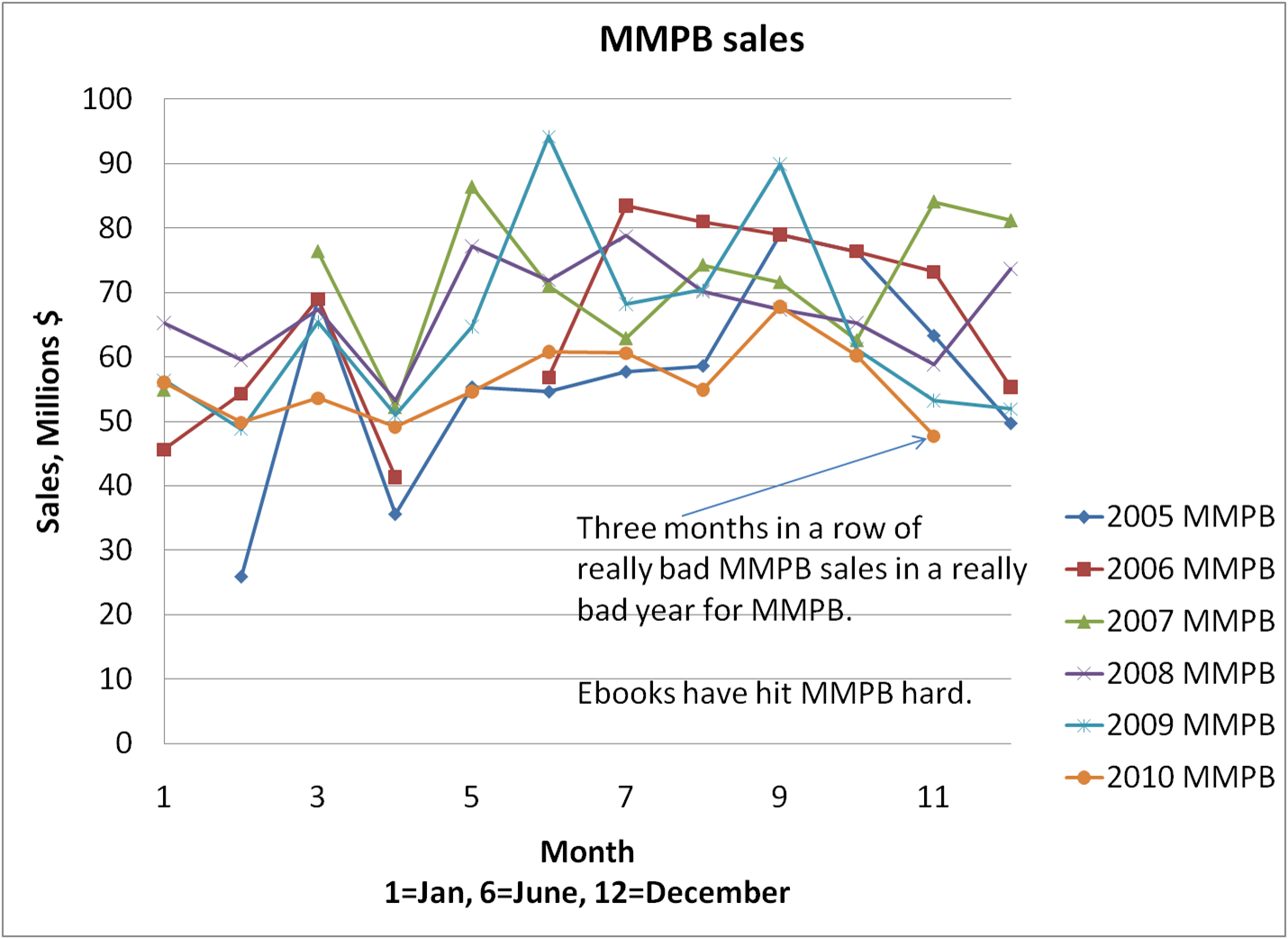

The last chart is the MMPB sales plot. MMPB sales have been weak and declining. I wonder how much of this is due to fewer MMPB sales at airports and to mass transit commuters. Anecdotal evidence is that road warriors and daily mass transit commuters have embraced ebooks early. Either way, this does not bode well for print midlist Romance, sci-fi, and other MMPB genres.

The graphs show one clear story. Ebooks are growing fast. Sadly, their growth is now taking the wind out of pbook sales now. It has only been obvious for a few months (per the data), but it is obvious that enough readers have made the transition to impact the bookstores. With the weakness in paperback and MMPB, I suspect midlist sales are being hit hard.

The only way I see reversing these trends is POD. I really wonder why B&N isn’t ripping out the CD/DVD section and putting in POD machines. Intense readers want variety. POD is the only way I see bookstores providing that variety. I have mostly read midlist authors. For those that love to read on paper, unless POD has a spectacular growth year in 2011, they will be driven to ebooks in 2012/2013.

What is the conclusion? The game has changed. The current bookstore model is broken. It almost doesn’t matter what the data is for December… The trend is that clear. Pbooks will have less variety in 2011 and at some point there will be a ‘tipping point.’ The only question is will that ‘tipping point’ be due to ereader growth or pbook contraction?

Got Popcorn?

Neil

Ps

The comments in my previous post have some very valid points on POD. I’m also waiting for Amazon’s quarterly report. I expect to find that we’re still seeing about 35,000 new books added to Kindle per month. But what if there is an upside? I hope you found it worth it to read this very long article.

Thanks for the data and analysis. Great stuff!

ReplyDeleteDavid